What is Estate Tax?

Estate Tax is a tax on the right of the deceased person to transmit his/her estate to his/her lawful heirs and beneficiaries at the time of death and on certain transfers, which are made by law as equivalent to testamentary disposition. It is not a tax on property. It is a tax imposed on the privilege of transmitting property upon the death of the owner. The Estate Tax is based on the laws in force at the time of death notwithstanding the postponement of the actual possession or enjoyment of the estate by the beneficiary.

Estate taxes are paid by the heirs, beneficiaries, executor, or the administrator in order to transfer property to beneficiaries or heirs upon the decedent’s passing.

How is estate tax determined?

Estate

tax

is calculated by first determining the value of the deceased’s net estate. This

is done by getting the difference between the deceased’s gross estate as

defined under Section 85 of the Tax Code, and the allowable deductions of the

decedent, which is defined under Section 86.

Net

Estate

= Gross Estate – Deductions

Gross Estate can be:

- Real properties, bank accounts (savings, joint, time deposit), stocks and other securities

- Personal property such as car, jewelry, works of art, furniture, etc.

Once the

values are established, the estate tax is easily established by referring the

amount to the BIR’s Estate Tax Table, which has been in effect since 1998.

Sample Presentation (say husband died) (Note: also applicable to your parents, siblings, relatives, etc. as

long as they have Gross Estate)

Example Gross Estate

- Real Estate Properties (House and Lot and Vacant Lot in Province) - P 7,000,000

- Personal properties (car, bank deposit/time deposit, stocks, etc.) - 3,000,000

Total - P 10,000,000

Example Deductions:

- Standard Deduction 1,000,000

- Family Home 1,000,000

- Funeral Expenses - 200,000

Net Estate = Gross Estate – Deductions- Medical Expenses 500,000

Total - P 2,700,000

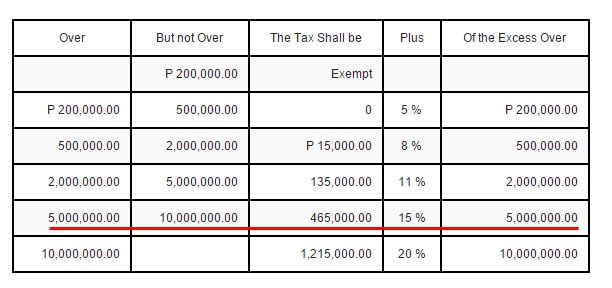

Tax due to be paid to BIR (refer below to BIR’s Estate Tax Table):

First P 5,000,000 - P

465,000

Next P 2,300,000 - P 345,000

Total TAX DUE - P 810,000 (this is the amount the wife will pay to BIR)

BIR Estate Tax Table (effective January 1, 1998 up to present)

1. Where does the wife will get P 810,000? Wife couldn’t withdraw their savings account /

What could have the husband and wife did to prevent this bad ordeal?

Can you escape paying Estate Taxes? NO!

1. When Bank Managers knew that the depositor died, depositor’s account will be automatically